The Best and Cheapest Homeowners Insurance in Wisconsin (2026)

Erie offers the cheapest home insurance in Wisconsin, at an average of $862 per year.

Compare Home Insurance Quotes in Wisconsin

Best Cheap Home Insurance in WI

To find the cheapest home insurance in Wisconsin, ValuePenguin collected thousands of quotes across more than 700 ZIP codes from 16 of the state's top home insurance companies.

To find the best insurance companies in WI, our experts compared each company's cost, customer service quality and coverage options.

Cheapest home insurance quotes in WI

Erie offers the cheapest home insurance rates in Wisconsin.

The company's average rate is $862 per year for $350,000 of dwelling coverage. That's $532 per year less than the overall state average, $1,394 per year.

Cheapest insurance companies

Compare Home Insurance Quotes in Wisconsin

If you have an expensive home, Wisconsin Mutual is one of the cheapest and best home insurance companies in Wisconsin. For $1 million in dwelling coverage, you'll pay an average of $1,222. That's around one-third of the Wisconsin state average.

Best cheap homeowners insurance in WI by dwelling coverage amount

What home insurance coverage do I need in WI?

Snow and tornados are two common weather events Wisconsin homeowners need to be ready for.

Most basic home insurance covers damage from both. However, if pipes are not protected properly from freezing cold temperatures your policy might not pay for the damage.

Best home insurance in Wisconsin for most people: Erie

-

Cost$862/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across WI. Read our methodology.

Best national company for Wisconsin homeowners: State Farm

-

Cost$970/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across WI. Read our methodology.

Best homeowners insurance for extra coverage in Wisconsin: America-Family

-

Cost$1,155/yrQuote is for $350,000 of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across WI. Read our methodology.

Best WI home insurance for an expensive home: Wisconsin Mutual

-

Cost$1,222/yr for $1 million in coverageQuote is for $1 million of dwelling coverage. This analysis used home insurance quotes for hundreds of ZIP codes across WI. Read our methodology.

Average home insurance cost in Wisconsin

In Wisconsin, the average cost of home insurance is $1,394 per year.

Average rates in Wisconsin are 35% cheaper than the national average cost of home insurance, which is $2,151 per year.

Average cost of home insurance in WI by dwelling coverage amount

Dwelling coverage | Annual cost |

|---|---|

| $200,000 | $900 |

| $350,000 | $1,394 |

| $500,000 | $1,843 |

| $1,000,000 | $3,345 |

Wisconsin home insurance is considerably cheaper than many neighboring states. In Minnesota, the average rate is $2,191 per year. In Illinois, it's $2,133 per year.

Homeowners insurance quotes in Wisconsin by city

Sheboygan, a lakefront town north of Milwaukee, has the cheapest home insurance in Wisconsin.

The average rate for a policy with $350,000 of dwelling coverage is $1,141 per year.

Osceola, a village on the St. Croix River and Minnesota border, has the most expensive rates at $1,719 per year. This may be because of the risks of river flooding. Many of the most expensive towns and cities are in the western part of the state near water sources.

Cost of WI home insurance by city

City | Annual rate | % from avg |

|---|---|---|

| Abbotsford | $1,388 | 0% |

| Abrams | $1,313 | -6% |

| Adams | $1,497 | 7% |

| Adell | $1,171 | -16% |

| Afton | $1,414 | 1% |

| Albany | $1,429 | 3% |

| Algoma | $1,272 | -9% |

| Allenton | $1,263 | -9% |

| Allouez | $1,247 | -11% |

| Alma | $1,490 | 7% |

| Alma Center | $1,433 | 3% |

| Almena | $1,602 | 15% |

| Almond | $1,448 | 4% |

| Altoona | $1,409 | 1% |

| Amberg | $1,345 | -4% |

| Amery | $1,672 | 20% |

| Amherst | $1,406 | 1% |

| Amherst Junction | $1,412 | 1% |

| Aniwa | $1,357 | -3% |

| Antigo | $1,348 | -3% |

| Appleton | $1,285 | -8% |

| Arcadia | $1,548 | 11% |

| Arena | $1,396 | 0% |

| Argonne | $1,351 | -3% |

| Argyle | $1,493 | 7% |

| Arkansaw | $1,544 | 11% |

| Arkdale | $1,485 | 6% |

| Arlington | $1,384 | -1% |

| Armstrong Creek | $1,365 | -2% |

| Arpin | $1,472 | 6% |

| Ashland | $1,437 | 3% |

| Ashwaubenon | $1,211 | -13% |

| Athelstane | $1,353 | -3% |

| Athens | $1,351 | -3% |

| Auburndale | $1,460 | 5% |

| Augusta | $1,460 | 5% |

| Avalon | $1,337 | -4% |

| Avoca | $1,468 | 5% |

| Babcock | $1,488 | 7% |

| Bagley | $1,546 | 11% |

| Baileys Harbor | $1,219 | -13% |

| Baldwin | $1,644 | 18% |

| Balsam Lake | $1,630 | 17% |

| Bancroft | $1,486 | 7% |

| Bangor | $1,450 | 4% |

| Baraboo | $1,428 | 2% |

| Barneveld | $1,389 | 0% |

| Barron | $1,606 | 15% |

| Barronett | $1,613 | 16% |

| Bassett | $1,392 | 0% |

| Bay City | $1,581 | 13% |

| Bayfield | $1,457 | 5% |

Rates are for a policy with $350,000 of dwelling coverage.

Milwaukee, the largest city in the state, has rates that are middle-of-the-road, only 3% more than the state average. Madison, the second-largest city, has average rates that are 8% cheaper than the state overall.

Best-rated Wisconsin home insurance companies

Erie and USAA are the best rated Wisconsin home insurance companies for customer service.

Both companies receive relatively few customer complaints and are well-rated by J.D. Power. They also were rated well by ValuePenguin's editors, who consider service metrics, coverage options and rates.

However, USAA is only available to people with military connections. That includes current servicemembers, veterans and qualifying members of military families.

Wisconsin home insurance company reviews

Company |

Rating

|

Complaints

|

|---|---|---|

| Erie | 5.0 out of 5 | Low |

| USAA | 5.0 out of 5 | Low |

| State Farm | 4.5 out of 5 | Average |

| Auto-Owners | 4.5 out of 5 | Low |

| AAA | 4.5 out of 5 | Low |

| Hastings Mutual | 4.0 out of 5 | Low |

| American Family | 4.0 out of 5 | Low |

| Badger Mutual | 4.0 out of 5 | Low |

| Chubb | 3.5 out of 5 | Low |

| Acuity | 3.5 out of 5 | Average |

| Farm Bureau | 3.0 out of 5 | High |

| Travelers | 3.0 out of 5 | Average |

| Allstate | 3.0 out of 5 | Average |

| Farmers | 2.5 out of 5 | Average |

| Wisconsin Mutual | 2.0 out of 5 | Low |

| West Bend | 1.5 out of 5 | Average |

It's crucially important to look at customer service reviews when looking for the best homeowners insurance in Wisconsin.

Good customer service means a smoother process when you need to replace things or fix your home after they are damaged. Bad customer service is not only frustrating, it might also lead you to spend more money out-of-pocket on repairs and replacement items if coverage details aren’t explained to you correctly.

What home insurance do I need in Wisconsin?

Damage from heavy snowfall and tornadoes are two of the most important things home insurance needs to cover in Wisconsin.

Fortunately, most home insurance will cover damage from both snow and wind.

Does WI home insurance cover snow damage?

Wisconsin sees a large amount of snowfall every year. Much of the state sees an average of 40 to 50 inches each year, with some areas getting more than 100 inches at times. Your home insurance will usually cover damage snow can cause to your roof or the rest of your home.

But you may not have coverage if you don't do enough to prevent pipes or other parts of your home from freezing. Your company may decide damage because of a broken pipe or to a pool was preventable.

Does home insurance in WI cover tornados?

Yes, most home insurance in the state covers damage from tornadoes. That's important if you live in Wisconsin because your home is more likely to be damaged by a tornado.

Wisconsin has had an average of 24 tornadoes per year since 1999, according to the National Weather Service.

Your insurance will most likely cover damage caused by the wind, flying objects and falling trees. But it never hurts to double check and consider extended replacement cost coverage, which will pay out more to rebuild your home if it's badly damaged.

How to get cheaper home insurance in Wisconsin

The best way to get cheaper home insurance in Wisconsin is to compare quotes from different companies, look for discounts and adjust your coverages.

Looking at multiple companies and comparing rates is usually the best way to make sure you're getting the lowest price for the home insurance you need.

Shopping around can really pay off. In Wisconsin, the gap between rates from the cheapest and most expensive home insurance companies n is $1,273 per year .

Just about every home insurance company will offer some home insurance discounts that can lower your bills.

The biggest discount usually comes from bundling aa car insurance policy with home coverage. You can also often get a discount on property insurance in Wisconsin from improving your home, like making it more resistant to fire.

If you lower your coverage limits or raise your deductible, you will almost always lower your home insurance quotes.

You should always keep in mind that your deductible needs to be low enough to pay in an emergency. If your deductible is higher, you'll get less money to repair your home if it's damaged.

The best way to lower your coverage limits is to look for any coverage extras you might not need. Just make sure your limits are high enough to pay the cost of rebuilding your home and buy new stuff it it's all damaged.

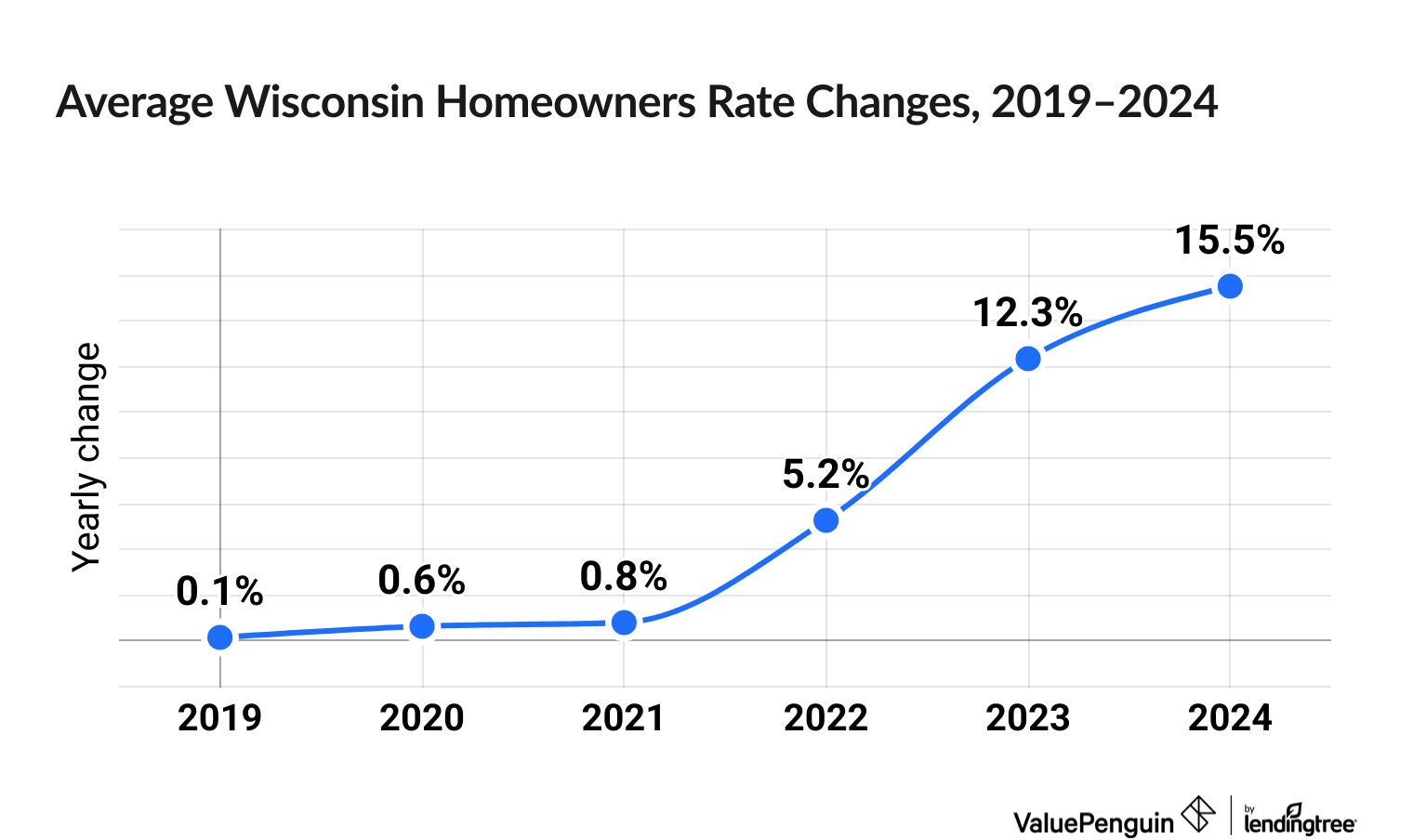

Wisconsin home insurance trends

Home insurance prices are up 38.7% in Wisconsin over the last six years.

Wisconsin homeowners have seen a sharp rise in their home insurance prices in recent years, jumping 12.3% in 2023 and 15.5% in 2024.

The biggest increase in home insurance prices among companies over the six-year period from 2019 and 2024 belonged to Farmers, which had an increase of 63.4%. Following closely behind were Liberty Mutual and Nationwide, at 57.9% and 56.8%, respectively.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

What is the best Wisconsin home insurance?

Eire and USAA have the best homeowners insurance in Wisconsin. Both have good customer service and cheap rates. However, you can only get USAA coverage if you're a military member or a qualifying family member.

What is the average cost of homeowners insurance in Wisconsin?

The average cost of homeowners insurance in Wisconsin is $1,394 per year. That's around $116 per month for $350,000 of dwelling coverage. The Wisconsin average is one third cheaper than the national average cost of home insurance, $2,151 per year.

Is homeowners insurance required in Wisconsin?

Home insurance isn't required in Wisconsin or in most other states. However, you'll almost always need a policy if you have a mortgage because your lender wants to protect a home it partially owns. It's also extremely risky not to have coverage.

What is the cheapest home insurance in Wisconsin?

Erie has the cheapest home insurance in Wisconsin, with an average rate of $862 per year for $350,000 of coverage. That's $532 per year less than the state average.

How much is home insurance in Milwaukee?

Home insurance in Milwaukee costs an average of $1,434 per year. That's 3% more expensive than the state average overall

Methodology

ValuePenguin collected and analyzed

To find the best homeowners insurance in Arizona, ValuePenguin collected quotes from 16 top companies across every residential ZIP code Wisconsin to find the cheapest rates. Quotes are for a 45-year-old married man with no prior insurance claims.

Coverage limits

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $5,000

- Deductible: $1,000

Rate information was collected using data from Quadrant Information Services. Prices are publicly sourced from insurer filings. They should be used for comparative purposes only.

Data from the J.D. Power customer satisfaction survey, the National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction survey, and ValuePenguin's ratings were combined to create home insurance ratings.

Snowfall statistics are from the National Weather Service as are Tornado statistics.

About the Author

Managing Editor

Ben Breiner is the Managing Editor of ValuePenguin/LendingTree's insurance vertical. He oversees a team of writers who focus on guiding readers through the rigors of home and auto coverage. He still loves that moment when the words fall together and he can translate an intimidating topic so a reader can make the best choice.

Ben got involved in insurance in 2021 when he joined ValuePenguin. He moved up from writer to editor and watched the team grow to expand the ways it helps consumers. Before that, he spent a decade as a sportswriter for newspapers in the Southeast and Midwest.

Ben had to put off buying his first car because of high insurance rates, so he's keenly aware how the wrong policy can get in the way of your goals. He should've shopped around and looked to the experts.

Insurance tip

Always keep an eye out for insurance you can load up on at a low price. A lot more liability coverage won't break the bank and protects your hard-earned assets.

Expertise

- Car insurance

- Home insurance

- Renters insurance

Education

- BA, Economics and Journalism, University of Wisconsin-Madison

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.