The Best Cheap Renters Insurance in Ohio

State Farm offers Ohio's cheapest renters insurance, at an average of $13 per month.

Compare Renters Insurance Quotes in Ohio

Best Cheap Ohio Renters Insurance

To pick the top renters insurance companies in Ohio, ValuePenguin's experts weigh price, coverage options, customer service and some of the unique values each company offers. The cheapest rates were found by compiling 193 quotes from eight companies across 25 of Ohio's largest cities.

Cheapest renters insurance in Ohio

State Farm has the cheapest renters insurance in Ohio.

With an average rate of $13 per month for $30,000 in personal property coverage, State Farm costs $15 per month less than the state average, which is $28 per month.

Cheapest insurance companies

Compare Cheap Renters Insurance in Ohio

State Farm also costs $5 per month less than the next-cheapest option, Lemonade. The average price of renters coverage in Ohio can differ by more than $40 per month. That's why it's important to compare quotes to make sure you're not paying too much.

Cheapest renters insurance companies in Ohio

Company | Monthly cost | ||

|---|---|---|---|

| State Farm | 4.5 out of 5 | $13 | |

| Lemonade | 4.0 out of 5 | $18 | |

| Amica | 4.0 out of 5 | $25 | |

| Progressive | 2.5 out of 5 | $25 | |

| Allstate | 2.5 out of 5 | $27 | |

| Assurant | 3.0 out of 5 | $29 | |

| Farmers | 3.5 out of 5 | $34 | |

| American Family | 3.0 out of 5 | $55 | |

Best Ohio renters insurance for most people: State Farm

-

Average cost for Ohio$13/moThis analysis used renters insurance quotes for 25 of the largest cities across the state. Full methodology.

Best for online experience in Ohio: Lemonade

-

Average cost for Ohio$18/moThis analysis used renters insurance quotes for 25 of the largest cities across the state. Full methodology.

Best renters insurance for customer service in Ohio: Amica

-

Average cost for Ohio$25/moThis analysis used renters insurance quotes for 25 of the largest cities across the state. Full methodology.

Ohio renters insurance rates by city

Toledo, an industrial city located in Ohio's northwest corner, has the most expensive renters insurance among the state's largest cities, at $42 per month.

The cheapest rates among Ohio's larger cities are in Middletown, which sits between Cincinnati and Dayton. The average rate in Middletown is $21 per month, half of Toledo's average.

Renters insurance in Columbus, the state's largest city, averages about $28 per month, just shy of the state average. The same is true of Cincinnati, where the average rate is $27 per month.

City | Monthly rate | % from average |

|---|---|---|

| Akron | $31 | 10% |

| Beavercreek | $27 | -3% |

| Canton | $28 | -2% |

| Cincinnati | $27 | -4% |

| Cleveland | $27 | -5% |

| Cleveland Heights | $27 | -5% |

| Columbus | $28 | -3% |

| Cuyahoga Falls | $27 | -3% |

| Dayton | $27 | -6% |

| Dublin | $27 | -5% |

| Elyria | $25 | -11% |

| Euclid | $27 | -6% |

| Hamilton | $23 | -20% |

| Lakewood | $22 | -24% |

| Lorain | $26 | -8% |

| Mansfield | $27 | -3% |

| Mentor | $27 | -5% |

| Middletown | $21 | -26% |

| New Albany | $26 | -7% |

| Newark | $21 | -25% |

| Parma | $25 | -11% |

| Springfield | $24 | -16% |

| Strongsville | $26 | -7% |

| Toledo | $42 | 48% |

| Youngstown | $31 | 8% |

Where you live can affect what you pay for renters insurance in a variety of ways. If a city has more property crime or more natural disasters, you'll likely pay more.

How to find the best renters insurance in Ohio

To find the best renters insurance coverage for you, first decide how much coverage you need, then shop around for quotes and weigh the quality of each company's customer service. The best renters insurance companies should be affordable while still providing the level of service and coverage you need.

You should start by figuring out how much renters coverage you need. You can do this by listing out what you own and how much you'd pay to get new belongings should they get damaged or lost.

The amount of coverage you choose to get will have a big impact on your renters insurance quotes. But don't skimp. You should get enough coverage to replace your property should it all be lost in an event like a house fire. If you don't, you'll likely end up paying more of your own money to refurnish your home than if you had gotten more coverage.

Comparing quotes from multiple companies is the best way to make sure you're getting a good deal. In Ohio, the most expensive company costs four times more than the cheapest. That means you can save a lot by shopping around.

Getting multiple quotes is also important because insurance companies calculate their rates differently. Where you live might matter most to one company, while others might more heavily consider your claims history. For this reason, your quote may end up looking different from that of your friends, family members or neighbors.

Pay attention to customer service reviews. If an emergency happens, your life will be much easier with better customer service.

For example, bad customer service can mean being forced to make extra calls or getting stuck on hold as you try to get answers about a claim. Doing that while trying to replace your belongings will only add to your stress. A company with good customer service might not put you through that.

What renters insurance do I need in Ohio?

Two of the more common natural disasters in Ohio are flash floods and tornadoes, and they might require extra coverage.

Does Ohio renters insurance cover flash floods?

Regular renters insurance won’t pay for damage caused by flooding. So you might have to get a flood insurance policy from either the government's National Flood Insurance Program (NFIP) or a private company.

Make sure your flood coverage matches the kind of home you’re renting. You don’t need to protect the structure of your rented home, only your things, so you likely won’t need a policy if you’re not living on the ground floor.

Does Ohio renters insurance cover tornadoes and wind damage?

Tornado and wind damage are almost always covered by regular renters insurance. That can include property outside your home, like a bike, or if a window is broken and debris is blown into the home you rent.

Ohio renters insurance trends

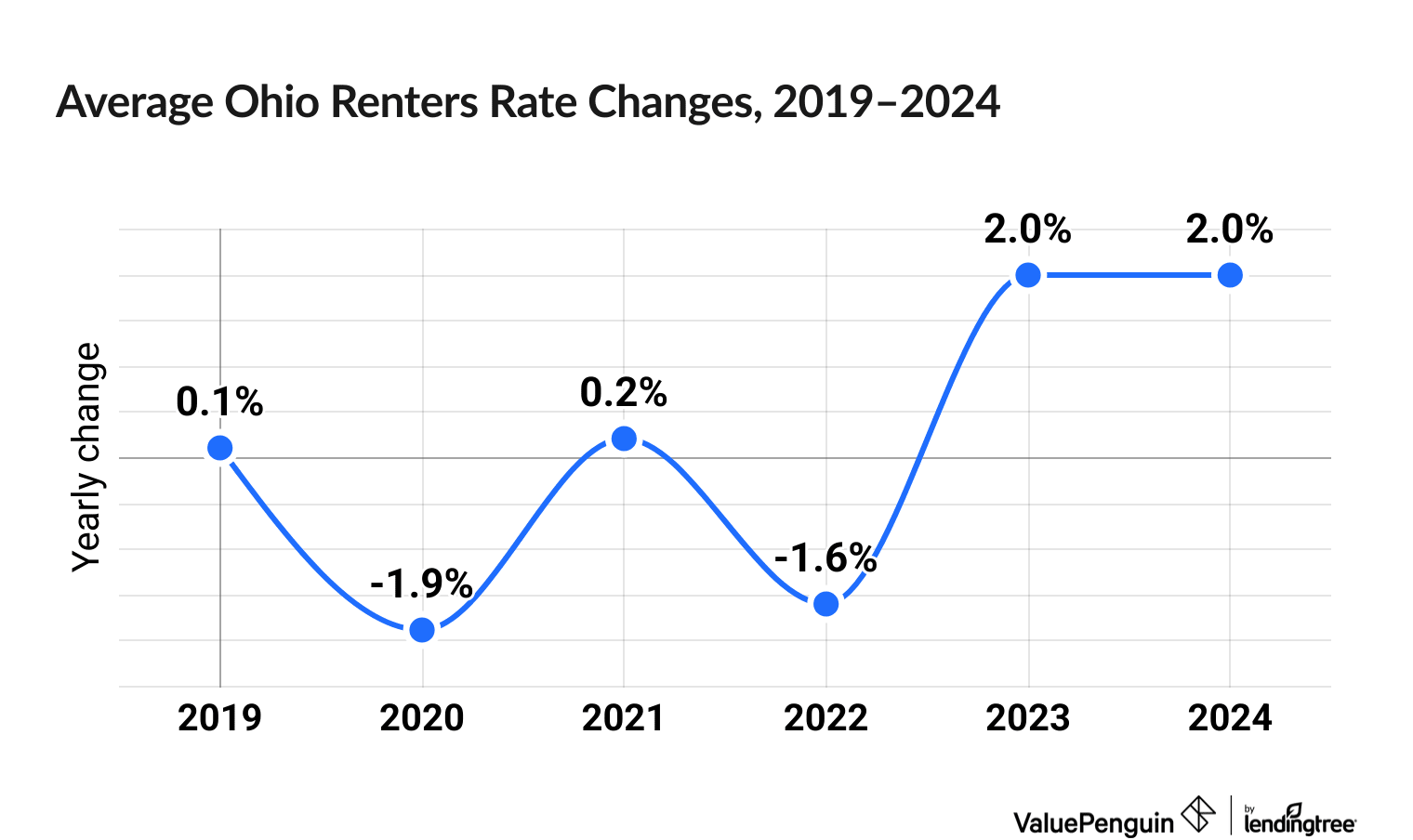

Renters insurance prices have gone up 0.8% in Ohio over the last six years.

Ohio renters insurance rates went up between 0.1% and 33.9% over the last six years, depending on the company.

Renters insurance prices, on average, actually decreased in 2020 and 2022, but then saw a slight uptick of 4.1% across 2023 and 2024.

Among the major OH insurers, the biggest increases have been at Farmers (33.9%), Travelers (15.5%) and USAA (15.4%).

Renters insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

How much is renters insurance in Ohio?

Ohio renters insurance costs an average of $28 per month. That makes it the eighth-most expensive state for rental insurance. It also has higher rates than any neighboring state except Michigan.

Can landlords in Ohio require you to get renters insurance?

Some landlords may put a requirement for renters insurance in the lease agreement that they present to you as a tenant. However, there's no state law that mandates all renters in Ohio must get renters insurance coverage.

How quickly can I get renters insurance?

In most cases, insurers are able to provide renters with coverage immediately, often called same-day renters insurance. But some companies make new customers wait at least one day as a way of fighting fraud. If your landlord has required renters insurance as a condition of your lease, you should make sure that you include their contact information in your insurance application so that they're listed as an interested party. That's how the insurer will notify your landlord of the policy.

How much renters insurance do you typically need?

In most cases, renters can get good value out of a policy by choosing $20,000 to $40,000 in coverage for personal property, along with the typical $100,000 in personal liability coverage. Other coverages such as loss of use are often calculated as a percentage of the personal property limit, so all you usually need to do is decide on that one number.

How much is renters insurance in Columbus, Ohio?

The average rate for renters insurance in Columbus, Ohio, is $28 per month. That’s slightly cheaper than the state average.

How much is renters insurance in Cincinnati?

In Cincinnati, the average rate for renters insurance is $27 per month. That’s 4% lower than the state average.

Methodology

To find Ohio’s cheapest renters insurance ValuePenguin gathered quotes from eight companies across the 25 biggest cities in the state. Quotes are for a 30-year-old woman who isn’t married, lives alone and has filed no recent claims.

Quotes include $30,000 of personal property coverage.

- Personal property: $30,000

- Personal liability: $100,000

- Medical payments: $1,000

- Loss of use: $9,000

- Deductible: $500

Star ratings for customer service are based on a proprietary metric that weighs the National Association of Insurance Commissioners (NAIC) complaint index, J.D. Power's annual customer satisfaction survey and ValuePenguin’s own editor's ratings.

About the Author

Managing Editor

Ben Breiner is the Managing Editor of ValuePenguin/LendingTree's insurance vertical. He oversees a team of writers who focus on guiding readers through the rigors of home and auto coverage. He still loves that moment when the words fall together and he can translate an intimidating topic so a reader can make the best choice.

Ben got involved in insurance in 2021 when he joined ValuePenguin. He moved up from writer to editor and watched the team grow to expand the ways it helps consumers. Before that, he spent a decade as a sportswriter for newspapers in the Southeast and Midwest.

Ben had to put off buying his first car because of high insurance rates, so he's keenly aware how the wrong policy can get in the way of your goals. He should've shopped around and looked to the experts.

Insurance tip

Always keep an eye out for insurance you can load up on at a low price. A lot more liability coverage won't break the bank and protects your hard-earned assets.

Expertise

- Car insurance

- Home insurance

- Renters insurance

Education

- BA, Economics and Journalism, University of Wisconsin-Madison

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.